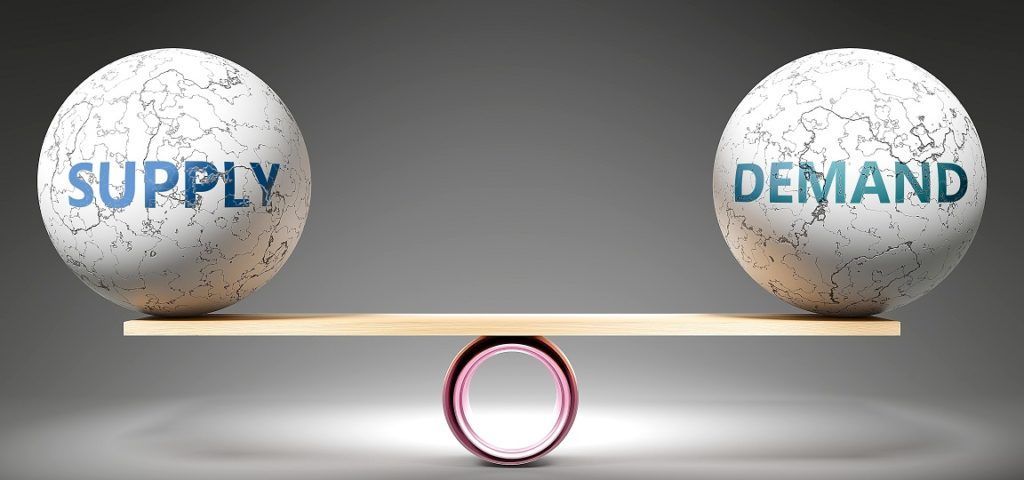

Supply and demand are the fundamental forces that drive a market economy. These two elements determine the price of goods and services, and how much of them will be available in the market. When both supply and demand interact, they create what is known as a market price or equilibrium price.

Supply refers to how much of a good or service producers are willing to sell at various price levels. Generally, as prices rise, producers are more likely to supply more of the product. For example, if a company can sell smartphones at a higher price, it is more motivated to produce more smartphones. The opposite is also true—if the price of a good falls, businesses may produce less of it because they make less profit.

Demand, on the other hand, refers to how much of a product or service consumers are willing to buy at different prices. Consumers usually want to buy more when prices are low, but when prices go up, they might cut back or stop buying. For example, if the price of coffee goes down, more people may buy it. But if the price of coffee rises, some consumers might switch to tea or drink less coffee.

The point where supply and demand meet is called equilibrium. At this point, the amount that producers want to sell is equal to the amount that consumers want to buy, and this sets the market price. If the price is too high, there will be excess supply, meaning that businesses have more goods than people are willing to buy. If the price is too low, there will be excess demand, meaning that more people want to buy the product than what is available.

Changes in supply and demand can occur for many reasons. For example, a new technology may make it cheaper to produce a product, increasing supply. Alternatively, changes in consumer preferences, income, or the price of related goods can affect demand. When supply or demand changes, it causes the market to move to a new equilibrium, where prices and quantities adjust to the new conditions.

Supply and demand play a critical role in determining how a market economy functions. By balancing the quantity of goods produced and consumed, these forces help allocate resources efficiently, ensuring that products are available at the right price for both consumers and businesses.

Post Comment